- Digital Age

- Distributed Energy Resources

- Energy Technologies

- Energy Technologies

- Energy Cloud

European Utilities Are Moving toward New Energy Platforms at Different Paces: Part 2

The energy industry is experiencing a profound transformation as the sector moves toward more intelligent, more distributed, and cleaner use of energy. Utilities’ traditional business models are being challenged by disruptive firms offering new services that leverage more advanced technology, as described in Guidehouse’s Energy Cloud analysis in its Navigating the Energy Transformation white paper. In the first post of this blog series, I described six new energy platforms underpinning the energy transformation. In this post and in the next post, I will show that some European utilities have been more active than others in partnering with, and investing in, companies offering new energy platforms. Finally, I will argue that in order to be successful in the transition toward a smarter, more digital energy future, utilities will need to strategically adopt the most relevant new energy platforms.

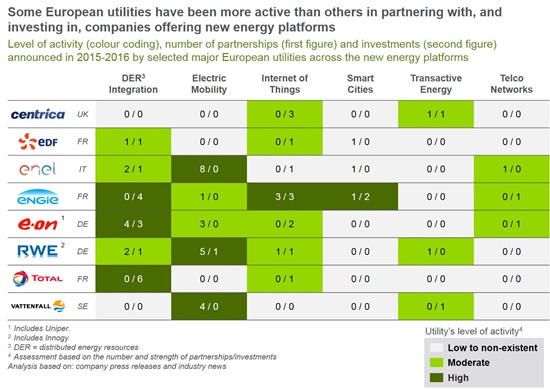

I analyzed the level of activity for eight of the largest European energy utilities engaging with companies offering new energy platforms. Partnerships, which often take the form of exclusive contracts, and investments, which are characterized as direct capital into companies, were grouped and assessed. Note that only partnerships and investments announced in 2015-2016 were included in the analysis; any previous announcements do not appear. The analysis also excludes any internally developed products and services that may fit in the new energy platforms.

(Source: Guidehouse, Inc.)

The matrix above provides a high level overview of the major European utilities’ strategic positioning within and across the six energy platforms. Distributed Energy Resources (DER) Integration and Electric Mobility are the two energy platforms with the highest level of activity from the major European utilities. Internet of Things (IoT) and Smart Cities are platforms where European utilities are more moderately active, while Transactive Energy and Telecommunications Networks feature the lowest level of activity. Of the eight European utilities covered, ENGIE, Total, and E.ON/Uniper are most active in DER Integration, while Enel, RWE/Innogy, and Vattenfall are most active in Electric Mobility. ENGIE also stands out as being particularly present in IoT and Smart Cities. Although Centrica and EDF appear to be relatively less active in new energy platforms, one should recognize that they have been developing new products and services internally rather than externally—an element that is not captured in this analysis.

The relative activity in partnerships versus investments varies across energy platforms. Electric Mobility activity consists almost entirely of partnerships—where companies prefer signing agreements with automakers and charging infrastructure developers. In contrast to some of the other platforms, utilities may not consider Electric Mobility to be a core business and so are less prone to directly invest in this new platform. This is the case of Enel with Nissan and RWE with Volkswagen. On the other hand, almost all of the European utilities’ activity with the IoT platform has been through investment. For example, Centrica acquired water leak detection and flow monitoring company FlowGem and added it to the Connected Home portfolio Centrica offers to British customers.

In the next post of this blog series, I will show that the majority of partnerships are with companies located in Europe, while most of the investments are made in organizations based in North America.